Getting sick or injured is stressful enough. The stress becomes even heavier when unpaid medical bills start arriving, and you do not know what will happen if you cannot pay them. Many people feel confused, scared, or tempted to ignore the notices, hoping the problem will somehow disappear. Unfortunately, unpaid healthcare charges rarely go away on their own.

In the United States, millions of patients struggle with healthcare costs due to high deductibles, insurance gaps, and unexpected emergency care. When bills remain unpaid, they can lead to collections, credit damage, and even legal action, creating long-term financial consequences that affect everyday life.

This guide explains exactly what happens when medical bills go unpaid, how they can impact your finances and credit, and what realistic options exist to manage or reduce the debt. Understanding the process is the first step toward regaining control and making informed decisions instead of reacting out of fear.

What Is Medical Debt?

Medical debt refers to unpaid healthcare charges that a patient owes after receiving medical treatment. This can include hospital stays, emergency room visits, surgeries, diagnostic tests, prescriptions, specialist care, and follow-up services. Even people with health insurance can end up with medical debt if their coverage does not fully pay for the care they receive.

In many cases, medical debt builds up because insurance plans require patients to pay deductibles, copayments, or coinsurance before coverage applies. Errors in claims processing or delays in reimbursement, often handled by medical billing services in the USA, can also contribute to unexpected patient balances when costs are not settled accurately or on time.

Medical debt affects a large portion of the U.S. population. Research shows that about 36 percent of U.S. households carry some form of medical debt, and more than 20% have past due medical bills. A significant number of patients are contacted by debt collectors over unpaid healthcare charges, and many owe thousands of dollars for a single medical event. These findings highlight how quickly medical costs can turn into long-term financial strain.

Unlike other types of debt, medical debt is usually unexpected. People do not plan for accidents, sudden illness, or emergency procedures. As a result, bills can arrive weeks or months later, often totaling thousands of dollars. When these balances are not paid on time, they move from simple unpaid charges to a larger financial issue that can affect credit, savings, and long-term financial stability.

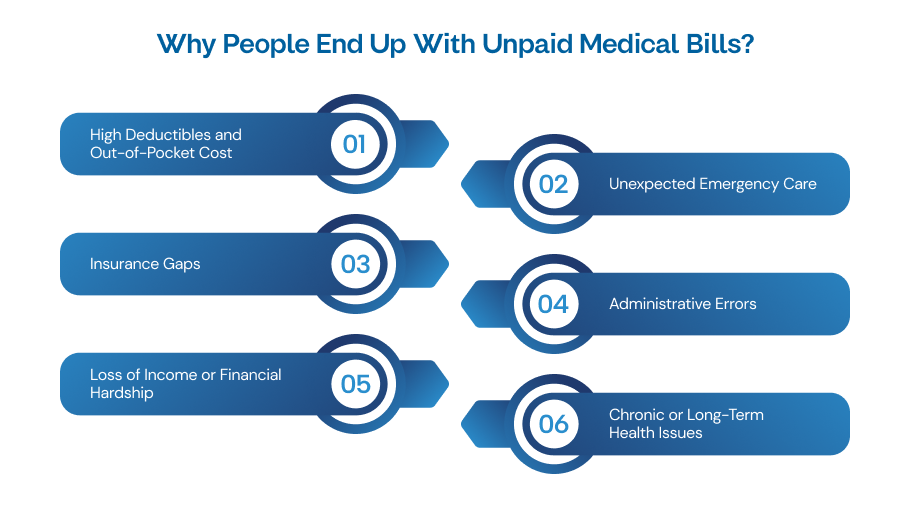

Why People End Up with Unpaid Medical Bills?

Many Americans struggle with medical bills even when they have insurance. There are several reasons why medical debt accumulates:

- High Deductibles and Out-of-Pocket Costs

Insurance plans often require patients to pay high deductibles before coverage begins. Coinsurance and copayments can also add up quickly. A single hospital visit or surgery can easily exceed these amounts, leaving patients with large balances.

- Unexpected Emergency Care

Emergencies do not come with warning. A sudden illness, accident, or urgent surgery can generate bills that are difficult to cover, especially if the patient is uninsured or underinsured.

- Insurance Gaps

Not all services are fully covered by insurance. Out-of-network care, denied claims, or procedures considered “non-essential” can result in surprise bills. Even routine testing can sometimes result in partial coverage.

- Administrative Errors

Mistakes in billing, coding, or claims processing can create unexpected charges. Errors such as duplicate billing, incorrect patient information, or unprocessed insurance claims can leave patients responsible for paying more than they expected. This is why working with a reliable medical billing services company is important. They help ensure claims are processed correctly and reduce the risk of unexpected balances.

- Loss of Income or Financial Hardship

Job loss, reduced work hours, or other financial emergencies can make it difficult to keep up with bills. When income drops, even modest medical costs can become unmanageable.

- Chronic or Long-Term Health Issues

Patients with ongoing medical conditions often face repeated bills for medications, therapies, and doctor visits. Over time, these costs accumulate, creating a steady burden that can lead to unpaid medical debt.

Can Hospitals Deny Medical Care If You Cannot Pay?

Many patients worry that hospitals will refuse treatment if they cannot afford to pay. In the United States, this is not the case for emergency care. Federal law, specifically the Emergency Medical Treatment and Labor Act (EMTALA), requires hospitals to provide stabilizing treatment for anyone facing an emergency, regardless of insurance status or ability to pay. Hospitals cannot turn patients away or let their condition worsen because of unpaid bills.

However, non-emergency care may be handled differently. Some hospitals and clinics may require payment or proof of insurance before scheduling elective procedures, routine checkups, or specialized treatments. That said, most healthcare providers understand financial hardship and often offer financial assistance programs, sliding scale fees, or payment plans to make care more accessible.

Working with medical billing experts can help patients navigate bills, verify coverage, and apply for assistance programs. Many practices outsource medical billing services to ensure claims are processed correctly, minimize errors, and prevent surprise balances from delaying future care.

What Happens If You Don’t Pay Medical Bills?

Unpaid medical bills can quickly lead to serious financial problems. When you miss payments, balances can grow, debt collectors may get involved, and your credit can be affected. The process usually follows a series of steps, from bills being sent to collections to potential legal actions or liens. Understanding these consequences helps you act early and manage the situation effectively.

- Medical Bills are Sent to Collections

When medical bills remain unpaid for 30 to 90 days or longer, healthcare providers may sell the debt to collection agencies. These agencies then take over the responsibility of recovering the amount owed. Collection agencies contact patients persistently through calls, letters, and emails, and they can negotiate payment plans. Their goal is to recover the debt efficiently, which can create stress and pressure for patients.

- Interest and Fees Begin to Accumulate

Unpaid balances often grow quickly due to interest rates and collection fees. Some providers also partner with medical credit cards or financing options that carry high interest. Over time, what started as a manageable bill can become significantly larger if not addressed promptly.

- Late Fees Are Added

Late fees are commonly applied when payments are missed, increasing the total amount owed. Provider policies vary, but even small fees can accumulate and make repayment more difficult. Staying in contact with the billing office can help prevent excessive charges.

- Debt Collectors Contact You

Debt collectors may reach out through phone calls, letters, and emails. While the Fair Debt Collection Practices Act (FDCPA) protects patients from harassment, collectors are allowed to communicate regularly and seek payment. Knowing your rights helps you manage these interactions effectively.

- Your Credit Score Is Impacted

Once medical debt goes to collections, it can appear on credit reports. This can lower your credit score significantly, affecting loans, credit cards, and other financial opportunities. Recent reporting changes mean some medical debt under $500 may no longer appear on reports, but larger unpaid bills can still have long-term consequences.

- You Can Be Sued for Unpaid Medical Bills

If bills remain unpaid, creditors may file a lawsuit. Statutes of limitations vary by state, limiting the time creditors can sue. If a court rules in their favor, you may receive a judgment requiring repayment.

- Wage Garnishment and Bank Levies

Court judgments can lead to wage garnishment, where a portion of your paycheck is taken to repay debt. Some states limit how much can be garnished. Bank levies are another method creditors use to recover unpaid balances directly from your accounts.

- Liens Can Be Placed on Property

A lien is a legal claim on assets like homes, vehicles, or other property. If medical debt remains unpaid, creditors may place a lien, affecting your ability to sell or refinance property. Liens can have long-term financial consequences until the debt is fully paid.

- Medical Debt After Death

Unpaid medical debt does not disappear after death. During probate, creditors can claim certain assets from the estate to settle balances. Some assets, such as life insurance or retirement accounts, are often protected, but other property may be used to repay debts, impacting heirs and beneficiaries.

How to Reduce or Manage Medical Debt

Managing medical debt can feel challenging, but taking proactive steps can reduce stress and help protect your finances. By carefully reviewing bills, negotiating charges, and using available resources, you can often lower the total amount owed and avoid long-term consequences. Small practices and patients alike can benefit from organized approaches and expert guidance.

Review and Audit Your Medical Bills

Start by requesting itemized bills for all services. Look for common billing errors, duplicate charges, or services you didn’t receive. Price comparison tools can help identify overcharges and ensure you are only paying what is fair. Even small practices can streamline this process by leveraging medical billing services for small practices to catch errors early.

Negotiate Medical Bills

Many providers offer discounts for self-pay patients, financial hardship, or lump-sum payments. Explaining your situation honestly can often reduce your overall balance. Negotiating directly with your provider may also prevent your account from being sent to collections.

Ask for a Hospital Payment Plan

If paying in full is difficult, ask your hospital about interest-free or low-interest payment plans. Make sure agreements are in writing to avoid misunderstandings and to protect your credit. Payment plans can keep your bills manageable and prevent collection actions.

Apply for Financial Assistance or Charity Care

Hospitals often provide financial aid programs, especially for patients who meet income requirements. Assistance may be available through ACA-related programs, nonprofit organizations, or specific hospital charity care initiatives. Applying early improves your chances of approval and reduces the financial burden.

Hire a Medical Billing Advocate

Medical billing advocates can review bills, identify errors, and negotiate on your behalf. Hiring one is particularly useful for complex cases or large bills. Partnering with professional medical billing services for small practices can offer similar benefits by ensuring accurate billing and helping patients navigate payment options.

Conclusion

Medical bills are more than just numbers on a statement; they can affect your financial security, mental well-being, and even access to care. The reality of medical debt shows how quickly unexpected costs can spiral, but it also highlights the importance of being proactive. From carefully reviewing bills to negotiating charges, setting up payment plans, and seeking professional guidance through medical billing services for small practices, there are ways to regain control.

The discussion around medical debt is not just about what happens when bills go unpaid; it’s about how individuals and small practices can navigate a complex system responsibly. By staying informed, asking questions, and using available resources, patients and providers alike can minimize the impact of medical debt. Facing the challenge head-on, rather than avoiding it, is the most effective strategy for protecting your financial health and peace of mind.

FAQs

- What counts as medical debt?

Medical debt includes unpaid charges for hospital visits, surgeries, emergency care, prescriptions, diagnostics, specialist care, and follow-up treatments. Even insured patients can owe money if coverage is partial or claims are delayed.

- Can unpaid medical bills affect my credit score?

Yes, if unpaid bills are sent to collections, they can appear on your credit report and lower your credit score. Recent reporting changes remove small debts under $500, but larger balances still impact credit.

- Can hospitals refuse treatment if I cannot pay?

Hospitals must provide emergency care regardless of your ability to pay, as per EMTALA. Non-emergency procedures may require proof of payment, but financial assistance programs and payment plans are often available.

- How can I reduce my medical debt?

You can review bills for errors, negotiate charges, request payment plans, apply for financial assistance, or hire a medical billing advocate. Small practices can also use medical billing services for small practices to manage billing accurately.

- What happens if medical debt remains unpaid?

Unpaid medical bills can be sent to collections, accrue interest and late fees, affect credit scores, result in legal action, wage garnishment, liens on property, or claims on estates after death.